The simple definition of a loan is ‘to borrow an amount of money for a certain period of time.’

You may take a loan from your family members, friends, and even from a financial institution like a bank. There are many reasons for taking a loan; it could be for your basic needs or purchasing a house, vehicles, etc.

However, you cannot borrow more than a certain amount from family or friends. That’s where banks and other financial departments come in.

Financial institutions offer huge loans, often with a long repayment period. On this financial assistance, the financial institutions charge a certain percentage of interest depending upon the amount and repayment schedule.

In the modern world, financial institutions provide financial assistance for personal loans to purchase vehicles, land and building houses, commercial loans for establishing new businesses, factories, farming, etc.

So, it’s extremely important to know how to make calculations related to your loans. But if you can’t do the calculations yourself, we have the best Percentages Calculator Loan that you can use right now.

How is Interest Charged on a Loan?

The inflation rate, service charges, and profit are the main determining factors of the interest rate. The longer the period of the loan, the greater will be the interest amount. The interest amount also depends on the loan amount.

There is a variety of loan amounts, repayment schedules, and rate of interest rates on personal and commercial loans. Whether it is a personal loan or a commercial loan, the loan period determines the total amount.

The repayment is usually made in monthly installments, and each installment includes a portion of the capital and interest.

Percentage plays an important role in determining the amount of loan payable in a monthly installment. There are different types of loans, and each has a different payment. The three types of loans are Interest-Only loans, Amortizing loans, and Credit Card loans.

But we’ll explain only the Interest-Only Loan with an example.

Interest-Only Loan Payment Formula

In the interest-only loan, you have to pay only the interest for the borrowed period while the principal balance remains unchanged. You can use our percentage calculator loan to find the payment within seconds. But you can do the maths yourself too.

To calculate payments for an interest-only loan, you have to take the following steps:

- In the first step, the annual interest rate (r) will be divided by the number of payments per year (n).

- In the second and final step, the obtained value will be multiplied by the amount you borrowed (a).

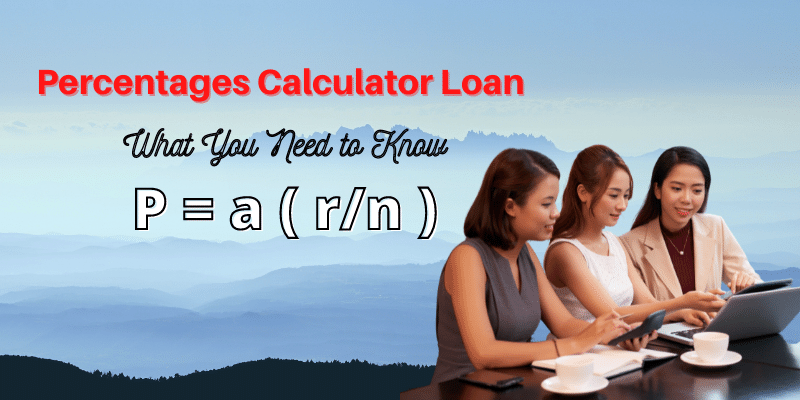

Here is the formula:

P = a ( r/n )

Example:

Suppose you have borrowed $150,000 at an interest rate of 8% for 25 years that will be repaid monthly. You can find the payments as:

Borrowed amount (a): $150,000

Interest rate (r): 8% expressed in number as 0.08

Payments per year (n): 12

Steps:

P = $150,000 ( 0.08/12 )

P = $150,000 ( 0.00667)

P = $1000

percentagecalculatorfree.com offers a range of free but highly reliable online calculators. We aim to make calculations easier for you. So, we have developed calculators in 4 categories, i.e., financial, math, chemistry, and others.

Our calculators can help you solve all of your calculation-related problems and provide you with the most accurate and precise calculations. You can find various percentage calculators on our website, including percentage calculator loans.

I love your blog, I would like a book from you.

Very interesting, certainly a very interesting way.